We use cookies to understand how you use our site and to improve your experience. This includes personalizing content and advertising. To learn more, click here. By continuing to use our site, you accept our use of cookies, revised Privacy Policy and Terms of Service.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

Here's Why Lowe's (LOW) Stock Gains More Than 40% in a Year

Read MoreHide Full Article

Lowe's Companies, Inc. (LOW - Free Report) looks well positioned to capitalize on demand in the home improvement market, backed by investments in technology, growth in the merchandise category and strength in Pro business.

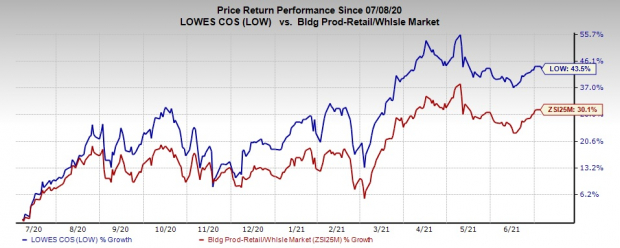

In addition, the company’s Total Home strategy, which includes providing complete solutions for various types of home repair and enhancement needs, appears encouraging. Impressively, shares of this renowned home-improvement retailer have surged 43.5% in a year, outpacing the industry’s 30.1% rally.

Let’s Delve Deeper

We note that Lowe's remains bullish on the home-improvement industry. It focuses on catering to consumers’ requirements for remodel activity, space-conversion projects as well as core repair and maintenance activity. During first-quarter fiscal 2021, comparable sales (comps) for the U.S. home-improvement business grew 24.4%, fueled by broad-based growth at all geographic regions and divisions.

In the fiscal first quarter, growth in lumber was quite impressive, aided by robust Pro demand and unusual inflation in the category. Apart from lumber, the company witnessed growth in areas of electrical, decor, kitchens, bath, and seasonal and outdoor living. Solid execution along with its compelling product offering helped it efficiently resonate with demand for the elevated home-related projects.

Image Source: Zacks Investment Research

Moreover, Lowe's is making constant investments in omni-channel capabilities to drive growth. It has been enhancing its omni-channel retailing capabilities in store operations, website and supply chain for sometime now to match customers’ demand. The company’s focus on perpetual productivity improvement or the PPI initiative is also steadily yielding results as it leverages store payroll by using technology to lower tasking hours, improve customer service and drive sales productivity. It also rolled out a secure mobile checkout to upgrade services in high-traffic areas.

Apparently, sales at Lowes.com surged 36.5% in the fiscal first quarter. This represents a 9%-sales penetration and a two-year comp of 146%. Digital sales benefited from customers’ shift toward online shopping. In the same quarter, the company closed the rollout of BOPIS lockers to 100% of its U.S. stores.

Lowe's Pro business is a significant growth driver. In fact, continued focus on the Pro category remains a key component of its Total Home strategy. In a bid to keep enhancing sales from pro customers, the company has been strengthening its pro-focused brands for a while now. It had earlier refurbished its pro-service business website LowesForPros.com to focus primarily on the needs of its Pro-customers. Markedly, pro sales surpassed the do-it-yourself category in the first quarter of fiscal 2021, registering above 30% comps growth.

Going forward, the Pro segment is expected to carry on the momentum with improved in-stock inventory levels, enhanced service offerings and its Pro loyalty program. Management is focused on boosting greater Pro penetration via the Pro Customer Relationship Management or CRM tool. The latest technology offers Pro desk with the tools to grow and retain Pro accounts via consistent and data-driven selling actions. Management is focused on expanding the company’s service levels in-store and online to address the needs of its Pro customers.

Wrapping up, Lowe’s is likely to sustain this solid growth trend on the back of the aforementioned robust strategic initiatives. A VGM Score of B with an expected long-term earnings growth rate of 13.7% further speaks volumes for this presently Zacks Rank #1 (Strong Buy) stock. You can see the complete list of today’s Zacks #1 Rank stocks here.

Other Solid Picks You May Look at

Tecnoglass (TGLS - Free Report) , currently a Zacks #1 Ranked stock, has a long-term earnings growth rate of 20%.

Beacon Roofing Supply (BECN - Free Report) delivered a substantial earnings surprise in the trailing four quarters, on average. It currently sports a Zacks Rank of 1.

Fastenal (FAST - Free Report) has an expected long-term earnings growth rate of 9% and a Zacks Rank #2 (Buy) at present.

Infrastructure Stock Boom to Sweep America

A massive push to rebuild the crumbling U.S. infrastructure will soon be underway. It’s bipartisan, urgent, and inevitable. Trillions will be spent. Fortunes will be made.

The only question is “Will you get into the right stocks early when their growth potential is greatest?”

Zacks has released a Special Report to help you do just that, and today it’s free. Discover 7 special companies that look to gain the most from construction and repair to roads, bridges, and buildings, plus cargo hauling and energy transformation on an almost unimaginable scale.

Image: Bigstock

Here's Why Lowe's (LOW) Stock Gains More Than 40% in a Year

Lowe's Companies, Inc. (LOW - Free Report) looks well positioned to capitalize on demand in the home improvement market, backed by investments in technology, growth in the merchandise category and strength in Pro business.

In addition, the company’s Total Home strategy, which includes providing complete solutions for various types of home repair and enhancement needs, appears encouraging. Impressively, shares of this renowned home-improvement retailer have surged 43.5% in a year, outpacing the industry’s 30.1% rally.

Let’s Delve Deeper

We note that Lowe's remains bullish on the home-improvement industry. It focuses on catering to consumers’ requirements for remodel activity, space-conversion projects as well as core repair and maintenance activity. During first-quarter fiscal 2021, comparable sales (comps) for the U.S. home-improvement business grew 24.4%, fueled by broad-based growth at all geographic regions and divisions.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

In the fiscal first quarter, growth in lumber was quite impressive, aided by robust Pro demand and unusual inflation in the category. Apart from lumber, the company witnessed growth in areas of electrical, decor, kitchens, bath, and seasonal and outdoor living. Solid execution along with its compelling product offering helped it efficiently resonate with demand for the elevated home-related projects.

Moreover, Lowe's is making constant investments in omni-channel capabilities to drive growth. It has been enhancing its omni-channel retailing capabilities in store operations, website and supply chain for sometime now to match customers’ demand. The company’s focus on perpetual productivity improvement or the PPI initiative is also steadily yielding results as it leverages store payroll by using technology to lower tasking hours, improve customer service and drive sales productivity. It also rolled out a secure mobile checkout to upgrade services in high-traffic areas.

Apparently, sales at Lowes.com surged 36.5% in the fiscal first quarter. This represents a 9%-sales penetration and a two-year comp of 146%. Digital sales benefited from customers’ shift toward online shopping. In the same quarter, the company closed the rollout of BOPIS lockers to 100% of its U.S. stores.

Lowe's Pro business is a significant growth driver. In fact, continued focus on the Pro category remains a key component of its Total Home strategy. In a bid to keep enhancing sales from pro customers, the company has been strengthening its pro-focused brands for a while now. It had earlier refurbished its pro-service business website LowesForPros.com to focus primarily on the needs of its Pro-customers. Markedly, pro sales surpassed the do-it-yourself category in the first quarter of fiscal 2021, registering above 30% comps growth.

Going forward, the Pro segment is expected to carry on the momentum with improved in-stock inventory levels, enhanced service offerings and its Pro loyalty program. Management is focused on boosting greater Pro penetration via the Pro Customer Relationship Management or CRM tool. The latest technology offers Pro desk with the tools to grow and retain Pro accounts via consistent and data-driven selling actions. Management is focused on expanding the company’s service levels in-store and online to address the needs of its Pro customers.

Wrapping up, Lowe’s is likely to sustain this solid growth trend on the back of the aforementioned robust strategic initiatives. A VGM Score of B with an expected long-term earnings growth rate of 13.7% further speaks volumes for this presently Zacks Rank #1 (Strong Buy) stock. You can see the complete list of today’s Zacks #1 Rank stocks here.

Other Solid Picks You May Look at

Tecnoglass (TGLS - Free Report) , currently a Zacks #1 Ranked stock, has a long-term earnings growth rate of 20%.

Beacon Roofing Supply (BECN - Free Report) delivered a substantial earnings surprise in the trailing four quarters, on average. It currently sports a Zacks Rank of 1.

Fastenal (FAST - Free Report) has an expected long-term earnings growth rate of 9% and a Zacks Rank #2 (Buy) at present.

Infrastructure Stock Boom to Sweep America

A massive push to rebuild the crumbling U.S. infrastructure will soon be underway. It’s bipartisan, urgent, and inevitable. Trillions will be spent. Fortunes will be made.

The only question is “Will you get into the right stocks early when their growth potential is greatest?”

Zacks has released a Special Report to help you do just that, and today it’s free. Discover 7 special companies that look to gain the most from construction and repair to roads, bridges, and buildings, plus cargo hauling and energy transformation on an almost unimaginable scale.

Download FREE: How to Profit from Trillions on Spending for Infrastructure >>