We use cookies to understand how you use our site and to improve your experience. This includes personalizing content and advertising. To learn more, click here. By continuing to use our site, you accept our use of cookies, revised Privacy Policy and Terms of Service.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

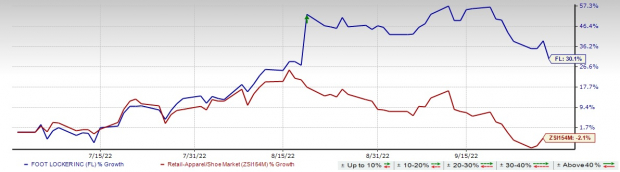

Foot Locker, Inc. (FL - Free Report) seems to be a good pick, thanks to its robust business strategies. Management has been investing significantly in reinforcing its digital presence and the direct-to-consumer (DTC) operations. FL is focused on improving performance through its operational and financial initiatives. Shares of this athletic footwear and apparel company have appreciated 30.3% over the past three months against the industry’s 2.1% decline.

Let’s Delve Deeper

Foot Locker is effectively managing inventory, investing in digital platforms and improving supply-chain efficiencies. The retailer has been augmenting its e-commerce platform, growing DTC operations, tapping into underpenetrated markets and opening Power Stores for a while. Management remains committed to the omni-channel progress.

In second-quarter fiscal 2022, FL’s digital sales penetration rate was 16.9%, up from 14.3% seen in fiscal 2019. In the first week of the fiscal third quarter, Foot Locker completed the global rollout of its new e-commerce platform via implementations in Singapore and Malaysia. Management had earlier activated a Shop My Store feature on its website. It also added Apple Pay and Google Pay to digital payment options for providing greater flexibility, and convenience to customers. FL’s buy online and pickup in-store capabilities along with an updated mobile-app experience appear encouraging.

Foot Locker is constantly accelerating its efforts, including greater diversification of merchandise and vendor mix, rollout of the important growth banners, advancement of omnichannel endeavors and implementation of the cost-savings program. FL announced a cost-optimization initiative, expecting the program to deliver $200 million of annual savings after being completely executed with the benefits starting in the fiscal third quarter and building into the fourth quarter. Image Source: Zacks Investment Research

International expansion is another major catalyst. Foot Locker continues to progress with its expansion strategy within Asia by penetrating the untapped markets via licensing arrangements. It is also advancing well with the membership program FLX, inspiring customers to remain within the Foot Locker portfolio of banners.

During the fiscal second quarter, the FLX program continues exhibiting momentum and helping Foot Locker serve customers efficiently. It has six key countries in Europe on the FLX platform. On its last earnings call, management informed that it captured above 70% of sales through its members in the United States, comparing favorably with the 50% witnessed two years ago.

Foot Locker anticipates capital expenditures of approximately $275 during fiscal 2022, directed toward store openings as well as technology and omnichannel investments. In fiscal 2022, management expects to open roughly 100 stores, including 40 community and power outlets, plus 20 WSS stores and two atmos stores, while shutting down nearly 190 stores.

Wrapping up, Foot Locker appears to be well-poised well for growth, based on all the aforementioned strengths. An impressive long-term expected earnings growth rate of 32.3% coupled with a Value Score of A shows the potential of this current Zacks Rank #3 (Hold) stock.

The Zacks Consensus Estimate for Designer Brands’ fiscal 2022 sales and earnings per share (EPS) suggests growth of 6.9% and 23.5%, respectively, from the corresponding year-ago levels. DBI has a trailing four-quarter earnings surprise of 55.1%, on average.

Buckle, a leading retailer of apparel, footwear and accessories has a Zacks Rank #2 (Buy) at present. BKE has a trailing four-quarter earnings surprise of 8.3%, on average.

The Zacks Consensus Estimate for Buckle’s fiscal 2022 sales and EPS suggests growth of 6.8% and 4.5%, respectively, from the year-ago corresponding figures.

Capri Holdings, a global fashion luxury group of iconic brands like Versace, Jimmy Choo and Michael Kors, carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for Capri Holdings’ current financial-year sales and EPS suggests growth of 3.3% and 10.1%, respectively, from the corresponding year-ago tallies. CPRI has a trailing four-quarter earnings surprise of 32.4%, on average.

See More Zacks Research for These Tickers

Normally $25 each - click below to receive one report FREE:

Image: Bigstock

Foot Locker (FL) Gains Above 30% in 3 Months: Here's Why

Foot Locker, Inc. (FL - Free Report) seems to be a good pick, thanks to its robust business strategies. Management has been investing significantly in reinforcing its digital presence and the direct-to-consumer (DTC) operations. FL is focused on improving performance through its operational and financial initiatives. Shares of this athletic footwear and apparel company have appreciated 30.3% over the past three months against the industry’s 2.1% decline.

Let’s Delve Deeper

Foot Locker is effectively managing inventory, investing in digital platforms and improving supply-chain efficiencies. The retailer has been augmenting its e-commerce platform, growing DTC operations, tapping into underpenetrated markets and opening Power Stores for a while. Management remains committed to the omni-channel progress.

In second-quarter fiscal 2022, FL’s digital sales penetration rate was 16.9%, up from 14.3% seen in fiscal 2019. In the first week of the fiscal third quarter, Foot Locker completed the global rollout of its new e-commerce platform via implementations in Singapore and Malaysia. Management had earlier activated a Shop My Store feature on its website. It also added Apple Pay and Google Pay to digital payment options for providing greater flexibility, and convenience to customers. FL’s buy online and pickup in-store capabilities along with an updated mobile-app experience appear encouraging.

Foot Locker is constantly accelerating its efforts, including greater diversification of merchandise and vendor mix, rollout of the important growth banners, advancement of omnichannel endeavors and implementation of the cost-savings program. FL announced a cost-optimization initiative, expecting the program to deliver $200 million of annual savings after being completely executed with the benefits starting in the fiscal third quarter and building into the fourth quarter.

Image Source: Zacks Investment Research

International expansion is another major catalyst. Foot Locker continues to progress with its expansion strategy within Asia by penetrating the untapped markets via licensing arrangements. It is also advancing well with the membership program FLX, inspiring customers to remain within the Foot Locker portfolio of banners.

During the fiscal second quarter, the FLX program continues exhibiting momentum and helping Foot Locker serve customers efficiently. It has six key countries in Europe on the FLX platform. On its last earnings call, management informed that it captured above 70% of sales through its members in the United States, comparing favorably with the 50% witnessed two years ago.

Foot Locker anticipates capital expenditures of approximately $275 during fiscal 2022, directed toward store openings as well as technology and omnichannel investments. In fiscal 2022, management expects to open roughly 100 stores, including 40 community and power outlets, plus 20 WSS stores and two atmos stores, while shutting down nearly 190 stores.

Wrapping up, Foot Locker appears to be well-poised well for growth, based on all the aforementioned strengths. An impressive long-term expected earnings growth rate of 32.3% coupled with a Value Score of A shows the potential of this current Zacks Rank #3 (Hold) stock.

Solid Picks in Retail

Some better-ranked stocks are Designer Brands (DBI - Free Report) , Buckle (BKE - Free Report) and Capri Holdings (CPRI - Free Report) .

Designer Brands, the leading footwear and accessories designer, presently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Designer Brands’ fiscal 2022 sales and earnings per share (EPS) suggests growth of 6.9% and 23.5%, respectively, from the corresponding year-ago levels. DBI has a trailing four-quarter earnings surprise of 55.1%, on average.

Buckle, a leading retailer of apparel, footwear and accessories has a Zacks Rank #2 (Buy) at present. BKE has a trailing four-quarter earnings surprise of 8.3%, on average.

The Zacks Consensus Estimate for Buckle’s fiscal 2022 sales and EPS suggests growth of 6.8% and 4.5%, respectively, from the year-ago corresponding figures.

Capri Holdings, a global fashion luxury group of iconic brands like Versace, Jimmy Choo and Michael Kors, carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for Capri Holdings’ current financial-year sales and EPS suggests growth of 3.3% and 10.1%, respectively, from the corresponding year-ago tallies. CPRI has a trailing four-quarter earnings surprise of 32.4%, on average.