We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

United Airlines (UAL) Plunges 24% in 3 Months: Buy the Dip?

Read MoreHide Full Article

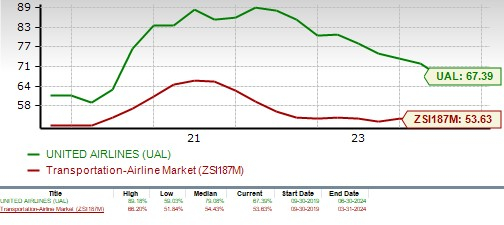

Shares of Chicago-based airline heavyweight United Airlines (UAL - Free Report) have not had a good time on the bourses of late, declining 23.8% in the past 90 days. The disappointing price performance resulted in UAL underperforming its industry’s 5.6% decline in three months. It also underperformed the S&P 500, of which the airline is a key member. However, UAL’s price performance compares favorably with that of fellow U.S. airline operators American Airlines (AAL - Free Report) and Delta Air Lines (DAL - Free Report) in the same timeframe.

Three-Month Price Comparison

Image Source: Zacks Investment Research

UAL is currently trading at a 25.8% discount to its 52-week high of $56.18, reached on May 16, 2024. In fact, United Airlines shares have plummeted more than 50% over the past five years and are currently trading at levels significantly below the pre-COVID levels. Additionally, this airline company’s stock has slipped below its 50-day moving average, which is an important indicator for gauging market trends and momentum. Falling below this average suggests a bearish trend, often prompting caution to investors.

50-Day Moving Average

Image Source: Zacks Investment Research

Given the significant pullback in UAL’s shares currently, investors might be tempted to snap up the stock. But is this the right time to buy UAL? Let’s find out.

Bearish Guidance for the September Quarter

Last month, United Airlines reported lower-than-expected revenues for the second quarter of 2024. Additionally, the airline’s earnings per share guidance for third-quarter 2024 was disappointing. Management attributed this to pricing pressure with excess capacity characterizing certain markets.

The practice of price cuts by low-cost carriers, as they struggle to fill the excess seats this summer, is hurting even bigger rivals. Discount carriers have added too many seats that they are now attempting to fill by lowering fares and compelling airline majors to do the same to stay competitive. This phenomenon dampened United Airlines’ pricing power. UAL’s management expects third-quarter 2024 adjusted earnings per share in the $2.75-$3.25 range. The Zacks Consensus Estimate was pegged at $3.61 at that time. UAL’s revenue miss was blamed on overcapacity related to summer flights.

Other Headwinds

Apart from pricing and top-line woes, the northward movement in operating expenses is hurting United Airlines’ bottom line, challenging its financial stability. In the first half of 2024, total operating expenses rose 5.7% year over year to $25.5 billion. The surge in operating expenses was primarily caused by an increase in labor costs and fuel expenses. Expenses on wages and benefits rose 14.2% in the same time.

The ongoing production cuts adopted by major oil-producing nations and geopolitical tensions are pushing up fuel costs. The average fuel price per gallon increased 3.8% year over year in the second quarter of 2024 to $2.76. We expect the metric to be $3.02 per gallon in the third quarter of 2024, reflecting an increase of 2.2% from third-quarter 2023 actuals.

We are also concerned about its high debt levels. The company’s times interest earned ratio of 2.9 at 2023-end compared unfavorably with the industry’s ratio of 4.6.

Long-Term Debt to Capitalization Image Source: Zacks Investment Research

Given the headwinds surrounding the stock, current-quarter as well as current-year earnings estimates are southbound, as shown below.

Image Source: Zacks Investment Research

Upbeat Air Travel Demand: A Saving Grace

Strong passenger volumes bode well for UAL. While air travel demand is particularly strong on the leisure front, business travel has also made an encouraging comeback. Driven by the air travel demand strength, UAL’s top line increased 7.5% year over year in the first half of 2024. This was driven by a 7.4% rise in passenger revenues.

From a valuation perspective, UAL is trading at a discount compared to the industry, going by the forward 12-month price-to-sales ratio. The reading is also below its median over the last five years. The company has a Value Score of A.

Image Source: Zacks Investment Research

To Sum Up

Agreed that the stock is attractively valued and upbeat passenger revenues are serving UAL well. However, given the abovementioned headwinds, we believe that it is not at all advisable to buy the dip in this Zacks Rank #3 (Hold) stock currently. Instead, investors should monitor the company’s developments closely for an appropriate entry point.

Image: Bigstock

United Airlines (UAL) Plunges 24% in 3 Months: Buy the Dip?

Shares of Chicago-based airline heavyweight United Airlines (UAL - Free Report) have not had a good time on the bourses of late, declining 23.8% in the past 90 days. The disappointing price performance resulted in UAL underperforming its industry’s 5.6% decline in three months. It also underperformed the S&P 500, of which the airline is a key member. However, UAL’s price performance compares favorably with that of fellow U.S. airline operators American Airlines (AAL - Free Report) and Delta Air Lines (DAL - Free Report) in the same timeframe.

Three-Month Price Comparison

UAL is currently trading at a 25.8% discount to its 52-week high of $56.18, reached on May 16, 2024. In fact, United Airlines shares have plummeted more than 50% over the past five years and are currently trading at levels significantly below the pre-COVID levels. Additionally, this airline company’s stock has slipped below its 50-day moving average, which is an important indicator for gauging market trends and momentum. Falling below this average suggests a bearish trend, often prompting caution to investors.

50-Day Moving Average

Image Source: Zacks Investment Research

Given the significant pullback in UAL’s shares currently, investors might be tempted to snap up the stock. But is this the right time to buy UAL? Let’s find out.

Bearish Guidance for the September Quarter

Last month, United Airlines reported lower-than-expected revenues for the second quarter of 2024. Additionally, the airline’s earnings per share guidance for third-quarter 2024 was disappointing. Management attributed this to pricing pressure with excess capacity characterizing certain markets.

The practice of price cuts by low-cost carriers, as they struggle to fill the excess seats this summer, is hurting even bigger rivals. Discount carriers have added too many seats that they are now attempting to fill by lowering fares and compelling airline majors to do the same to stay competitive. This phenomenon dampened United Airlines’ pricing power. UAL’s management expects third-quarter 2024 adjusted earnings per share in the $2.75-$3.25 range. The Zacks Consensus Estimate was pegged at $3.61 at that time. UAL’s revenue miss was blamed on overcapacity related to summer flights.

Other Headwinds

Apart from pricing and top-line woes, the northward movement in operating expenses is hurting United Airlines’ bottom line, challenging its financial stability. In the first half of 2024, total operating expenses rose 5.7% year over year to $25.5 billion. The surge in operating expenses was primarily caused by an increase in labor costs and fuel expenses. Expenses on wages and benefits rose 14.2% in the same time.

The ongoing production cuts adopted by major oil-producing nations and geopolitical tensions are pushing up fuel costs. The average fuel price per gallon increased 3.8% year over year in the second quarter of 2024 to $2.76. We expect the metric to be $3.02 per gallon in the third quarter of 2024, reflecting an increase of 2.2% from third-quarter 2023 actuals.

We are also concerned about its high debt levels. The company’s times interest earned ratio of 2.9 at 2023-end compared unfavorably with the industry’s ratio of 4.6.

Long-Term Debt to Capitalization Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Given the headwinds surrounding the stock, current-quarter as well as current-year earnings estimates are southbound, as shown below.

Upbeat Air Travel Demand: A Saving Grace

Strong passenger volumes bode well for UAL. While air travel demand is particularly strong on the leisure front, business travel has also made an encouraging comeback. Driven by the air travel demand strength, UAL’s top line increased 7.5% year over year in the first half of 2024. This was driven by a 7.4% rise in passenger revenues.

From a valuation perspective, UAL is trading at a discount compared to the industry, going by the forward 12-month price-to-sales ratio. The reading is also below its median over the last five years. The company has a Value Score of A.

Image Source: Zacks Investment Research

To Sum Up

Agreed that the stock is attractively valued and upbeat passenger revenues are serving UAL well. However, given the abovementioned headwinds, we believe that it is not at all advisable to buy the dip in this Zacks Rank #3 (Hold) stock currently. Instead, investors should monitor the company’s developments closely for an appropriate entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.